What’s Happening?

All news below is color-coded as “good“, “bad“, or “neutral” for mortgage rates.

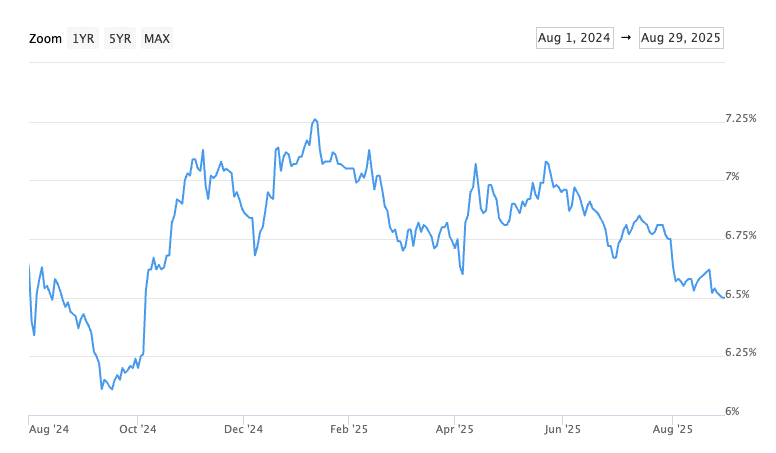

•Federal Reserve is will cut rates on 9/17 (good for rates): The Fed Fund futures market is still predicting an 87% chance that the Fed cuts rates by 0.25% on September 17th, AND, at least 1 more 0.25% cut by the end of 2025.

•Fed Data Pivot (good for rates): From Fed Chair Jerome Powell on August 22nd, “shifting balance of risks may warrant adjusting our policy stance.” That means “labor over inflation”. In other words, that 2% inflation target we’ve been hearing about for years is no longer the primary metric the Fed is watching. Instead, they are watching for weakness in the labor market to support rate cuts. And that weak jobs report and jobs revision released on August 1st was all they needed.

•Inflation Report (bad for rates): The July CPI (Consumer Price Index) and PPI (Produce Price Index) reports were released mid-August. The CPI was somewhat tame but is creeping higher, and just like in June, it showed a 2.7% year-over-year increase (we were sitting around 2.4% for much of 2025). Markets shrugged this data off.

PPI was a bit more alarming, showing that the PPI rose 0.9% in July alone, which, annualized, would be 10% per year. This is a large spike compared to 0% in June and 0.4% in May, so we are not actually seeing 10%/yr in PPI. That’s just the power of almost 1% in a single month if that trend were to continue, which is unlikely. This suggests that tariffs are pushing prices up, but so far, producers are eating the cost. Rates spiked at this news but have since dropped.

I think consumers will soon pick up the inflation tab, and to share my own anecdote, I’ve been shopping for new kitchen appliances and a sales rep at Pacific Sales shared how they’ve seen a lot of prices increase these last few months and they’re being told is due to the tariffs. I’m not sure how to fact check that one, but it’s worth sharing.

•Jobs Report (reported in my last email) (good for rates): The July BLS Labor Report released on August 1st and signaled a weaker-than-expected labor market with big revisions for May and June.

- New jobs in July came in much lower than expected at 73k new jobs; 100k were expected.

- More importantly, May and June were over-reported and are now revised down cumulatively by 258,000 jobs. This flies in the face of the “better-than-expected” reports we got in May and June which should have actually been worse-than-expected.

- Unemployment stayed at 4.2%.