What’s Happening?

All news below is color-coded as “good“, “bad“, or “neutral” for mortgage rates.

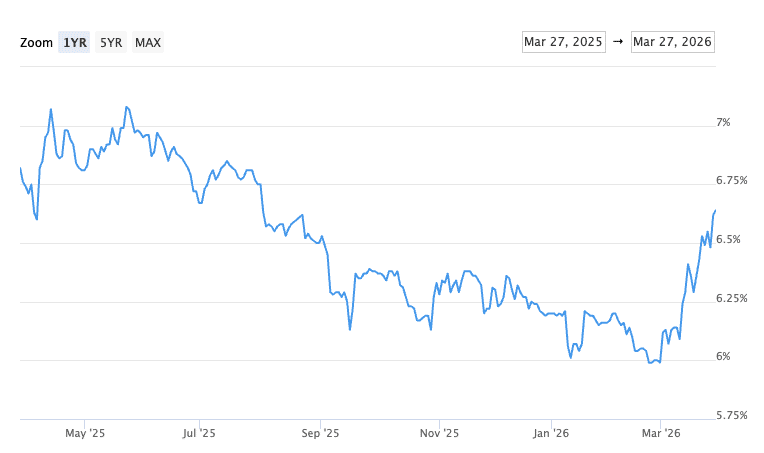

“Where oil prices go, so go rates.”

•Geopolitics (VERY bad for rates): The weekend of March 1st, the USA and Israel launched joint military operations and airstrikes against Iran. Iran retaliated with their own missile & drone attacks and has effectively closed the Strait of Hormuz waterway to any ships seeking passage. Roughly 25% of the world’s supply of oil & petroleum products passes through the Strait. This has sent the price of Brent Crude skyrocketing up from $70/barrel to over $110/barrel. Rising oil prices affect virtually all other prices and cause all rates (including mortgage rates) to rise sharply.

The last month of escalations has seen little in the way of talks of peace or a ceasefire, and rates will continue to worsen until so. This conflict and its effect on oil prices are the primary drivers of the recent rate rise.

•March Federal Reserve Meeting (bad for rates): The Federal Reserve met in the 3rd week of March. They left their funds rate unchanged, but Fed Chair Powell said that inflation was proving to be a problem that just wouldn’t go away, even without the Iran conflict and rise in oil prices. That has markets a little spooked and futures markets are predicting no more rate cuts until September, even then, the likelihood is small. Rate forecasts 6 months out are worthless, so consider that as meaning “no more rate cuts until further notice”. Oil will remain a big factor, which is influenced by the war in Iran, so I’ll be watching that closely to get a pulse on what’s to come.

•Jobs Report (neutral for rates): February’s jobs report showed that we LOST 92k jobs; a huge miss. New jobs were projected at +50k. Healthcare was a large driver in this, reflecting strike activity amongst Kaiser workers in CA and HI that ended in February. We should see a jobs rebound next month. In a normal world, a report like this would have also pushed rates down but all eyes are on oil prices and Iran for the time being.

•Unemployment Metric (good for rates): Unemployment in February ticked up from 4.3% to 4.4%. Weak labor market = dropping rates (usually), since Fed cuts are supported by weak labor market data.

•Inflation Report (neutral for rates): February’s CPI (inflation) report shows the CPI is back down to 2.4%. Prices are still rising, just slower… We’ve seen a 2.4% print only 4 times since 2021, though with oil prices up, I’m afraid the March report will show rising inflation again. Lower CPI = lower rates (usually), so a higher CPI next month will likely keep pushing rates up.