What’s Happening?

All news below is color-coded as “good“, “bad“, or “neutral” for mortgage rates.

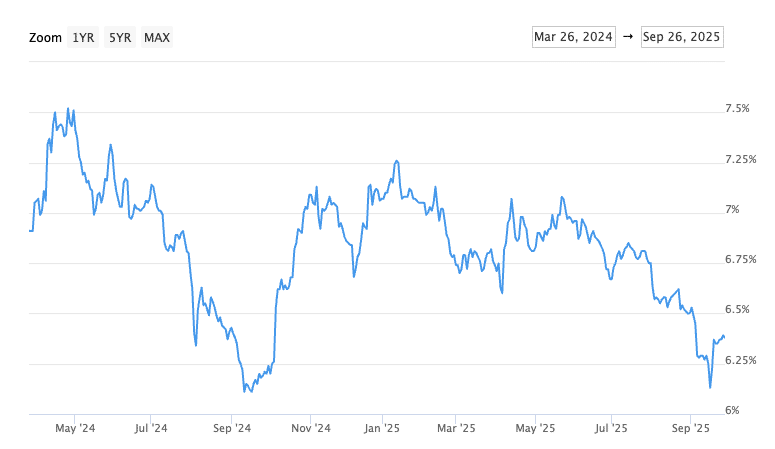

•Federal Reserve cut rates on 9/17 and will cut 1-2 more times in 2025 (neutral for rates): The Fed cut rates on 9/17 and will likely cut again on 10/29 & maybe once more on 12/10. After that, it’s unclear. I have this marked as “neutral for rates” is because long-term inflation seems to be stubbornly pushing back up which will push mortgage rate rates up. However, average mortgage rates are 1% lower now than they were in January, so we’ve come down a lot since then, but further drops are unlikely to be expected unless we see spikes in unemployment and a drop in the inflation rate.

•Fed Data Pivot (good for rates): Repeating what I wrote last month since it’s still relevant. The Fed is now watching the labor market (new jobs and unemployment) to influence its rate policy. “Labor over inflation” as Powell put it. We’ve had weak jobs and rising unemployment for a few months now. This may give the Fed the data they need to keep cutting rates.

•Jobs Report (good for rates): The August BLS Labor Report released the 1st week of September was a HUGE miss.

- New jobs in August came in much lower than expected at only 22k new jobs; 73k were expected. This compounds on top of the huge jobs report miss in July.

- There were some revisions to June and July jobs numbers previously reported; -27,000 & +6,000 respectively.

- Poor jobs numbers are currently the primary driver of lower mortgage rates.

Unemployment increased from 4.2% to 4.3%.

•Inflation Report (bad for rates): The August CPI (Consumer Price Index) and PPI (Produce Price Index) reports were released mid-September. The CPI spiked again; from 2.4% in most of 2025, to 2.7% in July, and now 2.9% in August (year-over-year). This is the highest we’ve seen in 2025.

Rising rents (shelter index) were the largest factor for this higher CPI. Rents increased at 0.4% month-over-month and are up nationally by 3.6% over the past 12 months.