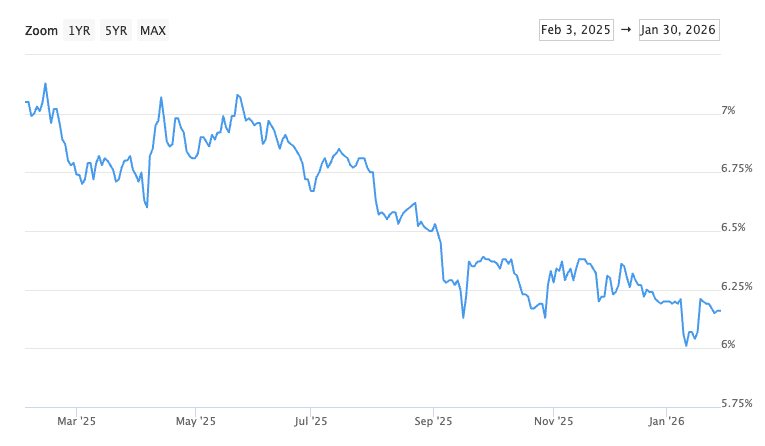

What’s Happening?

All news below is color-coded as “good“, “bad“, or “neutral” for mortgage rates.

•Mortgage Backed Securities Purchase (good for rates): On January 8th, Trump declared he’s ordering the purchase of $200B worth of mortgage-backed securities (MBS). If this happens, more MBS demand means lower mortgage rates. Rates fell 0.125% the next morning but quickly recovered as the news hype died off. If an actual MBS purchase plan is announced, expect rates to drop.

•Next Fed Rate Cut (bad for rates): The Federal Reserve had its first meeting of 2026 and left rates unchanged as expected. Markets don’t expect the next rate cut until the 2nd half of 2026, though I’ve noticed that when projections are more than a few months out, expect them to change.

In other Fed news, current Fed Chair Jerome Powell’s term is up in May this year and Trump has indicated he will nominate Kevin Warsh as the next Fed chair. This is an interesting choice since, during the post-2007 market crash, Warsh was resistant to cutting rates, and Trump has stated he wants a Fed Chair who supports rate cuts. I actually think this could be a good thing. If the Fed maintains its independence and remains data-driven, markets (and mortgage rates) will stay stable. Warsh could be a Chairman who supports market stability.

•Geopolitics (can be good or bad for rates): This month has been busy geopolitically in Venezuela and Greenland.

The U.S. forces captured Venezuelan leader Nicolás Maduro on Jan 3rd, which didn’t directly affect mortgage rates, but does add some uncertainty to markets. Uncertainty commonly causes rates to fall slightly, but we’re not seeing that here yet.

Trump indicated that the US was going to take control of Greenland and impose more tariffs until a deal was reached, which spooked markets. A few days later, markets calmed after Trump claimed a “framework of a future deal” was reached (which would avoid tariffs). We’re still awaiting details on what that means, and we’ll need those details soon to appease markets and address tariff worries, but for now, all is calm.

•Jobs Report (good for rates): The December BLS jobs report and showed 50k new jobs created, a little less than expected. A weak labor market can support rate cuts.

•Unemployment Metric (bad for rates): unemployment dropped to 4.4% compared to from 4.6% last month (can push rates up). A strong labor market can lead to fewer rate cuts whcih cancles out the dynamic from the jobs report above.

•Inflation Report (neutral for rates): December’s inflation report showed the CPI, year-over-year, is again sitting at 2.7%, the same annual increase we saw in November’s report. Food (groceries and restaurants combined) and natural gas prices were the heavy hitters since November, up 0.7% and 4.4% in 1 month, respectively. Yearly, those items are up 3.1% and 10.8%. While the overall index is steady, some rising categories hint at rising inflation again. This doesn’t really push rates up too much, but it has pushed the next expected Fed rate cut from April 2026 to June 2026. If January’s CPI report shows inflation rising, which can contribute to rising mortgage rates.