What’s Happening?

All news below is color-coded as “good“, “bad“, or “neutral” for mortgage rates.

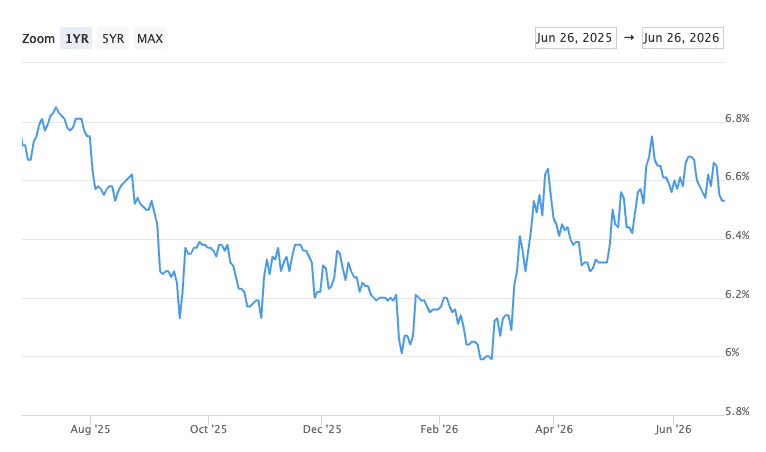

Summary: Just like my update last month, rates ended the month where they started. But that doesn’t mean nothing happened. Rates swung as much as 0.25% as economic and geopolitical factors impacted markets. Read on for more details.

•Geopolitics (good for rates): We end June with a Memorandum of Understanding (MOU) between the US and Iran, a 60-day ceasefire, and a 60-day period of toll-free passage through the Strait of Hormuz. Traffic through the Strait is picking up faster than expected. Initial projections were that it could take months for Strait traffic to ramp back up, but the International Energy Agency reported that the UAE is exporting oil at nearly 85% of pre-conflict levels.

•Brent Crude Oil Prices (good for rates): The MOU was signed on June 17th and Brent Crude Oil prices responded preemptively to the signing, falling from $84 at the end of May, to $77/barrel on June 17th, and have continued to fall since the signing, currently at $72.85. This is down from a high of $120 in late April, up from $65-70 before the war. Falling oil prices bring downward pressure on mortgage rates.

•Federal Reserve Action (bad for rates): Despite the drop in oil prices, we have a countervailing force that seems to have kept rates from falling back towards their early 2026 lows when conventional rates hit 5.99%. The Federal Reserve met last week and the expectation of Fed actions has changed over the last few months, from a possible rate cut in early 2027, to a possible rate hike in early 2027, and now to an expected rate hike as early as September of this year. The Fed Fund Futures market has that pegged at a 60% probability, far from a sure thing, but it’s a change in course regardless. The Fed hikes rates, in part, due to mounting inflation concerns. This prolonged increase in oil prices still needs to work its way through the economy and there is 1 more Fed meeting in July (rates expected to remain unchanged), so we have time to see a couple more months of market data. But, for now, this expectation is likely keeping mortgage rates a bit elevated.

•Inflation Report (bad for rates): The May CPI inflation report shows the CPI is up to 4.2%, meaning overall prices are up 4.2% since last year. Last month, the 12-month CPI ending in April was 3.8%, and 3.3% the month before. The driver of this 4.2% print is the increase in energy costs, mainly fuel oil and gasoline, which are up 40% in aggregate since May 2025. Now that oil has fallen to pre-war levels, CPI is likely to drop near 3% again in the coming months

•Jobs Report (bad for rates): The Jobs report covering May shows that 172k new jobs were added, soaring past the 82k expected new jobs. Even more surprising were the revisions to past months’ job numbers. March was revised up by 29k, April was revised up by 64k; 93k in positive revisions. These 3 months of positive job growth numbers and the wholesale inflation rate (what businesses pay other businesses for goods and services) in April rising to 6%, are contributing to sooner and sooner rate hike expectations.

•Unemployment Metric (neutral for rates): Unemployment in May again remained at 4.3%. There hasn’t been any meaningful change in this metric in 2026, having little effect on rates. 4.3% is considered a low unemployment rate when looking at data since 1948, ranging from 2.5% in 1953 to 10.8% in 1982. Unemployment hit a recent high of 10% in 2009 (ignoring the self-inflicted unemployment spike in 2020).